Notebook 009 - Cash Needs a Thesis

Wednesday was not a day where the desk failed to read the market.

That is what makes it useful.

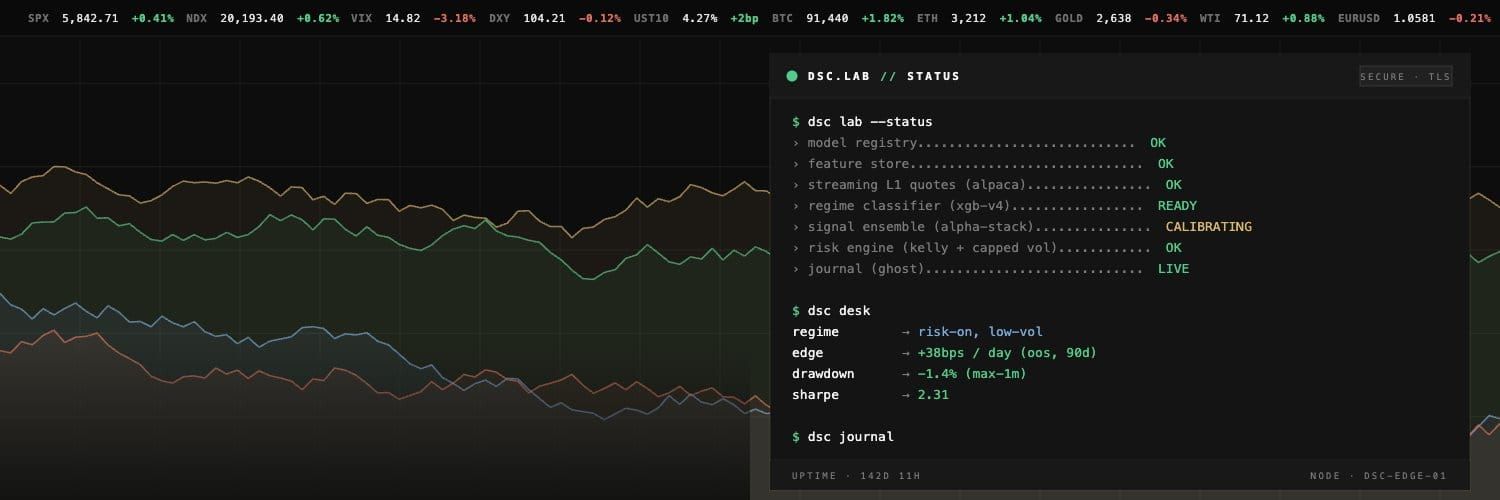

The broad tape was firm. The market stack was constructive. Semis and high-beta names had leadership. Volatility was calm enough to support risk. The plan did not ignore that. Onyx took approved trades, managed recovery positions, respected the no-loss rule, and ended the review window with a green day.

By most practical standards, that is a good paper-trading session.

And still, the desk left a question on the table: if the tape was that constructive, why was so much capital still waiting?

This is not financial advice. This is a notebook about building an operating process. The point is not whether a single day made enough or too little. The point is that Wednesday exposed a cleaner version of a problem that is easy to miss when the account is green. Sometimes the system does not fail by taking the wrong trade. Sometimes it underperforms by taking too little of the right environment.

Cash is protection. Cash is flexibility. Cash is patience.

Cash is also a position.

01 - A Good Day Can Still Teach A Hard Lesson

The easiest days to review are the obvious failures. A bad entry, a stale feed, a missing order, a broken rule. Those are painful, but at least the arrow points somewhere.

Wednesday was quieter than that. The executor did the thing it was supposed to do. It stayed inside the approved plan. It did not buy watch-only names just because they were moving. It did not lower sell targets below entry to make the book look cleaner. It did not treat a bullish screen as permission to freelance.

The recovery side worked. Existing positions were treated as first-class problems, not background clutter. Above-entry exits were active where they needed to be. When the tape gave recovery opportunities, the desk took them.

The fresh-risk side also worked. The names that were explicitly approved for new entries had clean enough behavior to complete profitable cycles. The plan had named them before the fact. The trader executed them after the fact. That is the correct order.

So the lesson is not that Onyx was broken.

The lesson is that a correct plan can still be undersized for the day it gets.

That distinction matters. If the plan is wrong, we fix the plan. If the execution is wrong, we fix the code. But if the plan is right and still too small, the next question is about capital allocation. That is a different muscle.

02 - The Book Came First

Every morning starts with the book we actually have.

That sounds obvious until there are fresh opportunities on the screen. Then the temptation is to treat open positions as old news and make the new watchlist feel like the real work. In a no-loss system, that is backwards. Existing positions are not leftovers. They are live commitments. They consume capital, attention, and risk capacity until they are resolved.

Wednesday got that part right.

The desk started with recovery management. Positions that had carried forward were reviewed, target orders were checked, and the system kept those targets above average entry. That is the non-negotiable rule doing its job in a practical way. It does not make drawdown disappear. It keeps the system from converting a temporary problem into a realized loss without permission.

But a no-loss book creates a second responsibility: the desk has to know how much fresh risk it can still responsibly add.

If the open book is heavy, staying cash-rich may be the right call. If the market backdrop is conflicted, holding back may be the right call. If macro or geopolitical risk is flashing, patience may be the right call.

The key phrase is "the right call."

Not the default. Not a habit. Not a vague feeling that more cash is safer.

Cash needs a reason the same way a trade needs a reason.

03 - Protection Can Become Drag

The operating model has been built around discipline. That was necessary. Early in a system's life, the danger is usually excess freedom: too many trades, too many interpretations, too much "it looks good" masquerading as a process.

Onyx has moved past the first version of that problem. The trader is not randomly inventing positions. The daily plan matters. The dashboard makes the book visible. The journal makes the misses hard to hide.

Once that foundation exists, a new problem appears.

The same caution that protects the desk can also keep it underexposed when the tape is paying for selective risk.

Wednesday was not a clean all-in day. There was still fragility in the backdrop. Oil and policy headlines were enough to keep the word "fragile" attached to the risk-on read. That matters. The answer was not to throw every brake away and call it conviction.

But the market was also not neutral. Breadth was better. Semis were working. Several names on or near the desk's universe confirmed strength. Approved fresh-risk candidates did what the plan hoped they would do. The book had evidence, not just a green label.

That is where under-deployment becomes measurable.

If the market stack is supportive, the best approved names are working, volatility is not fighting the tape, and the desk still has most of its capital idle, the system needs to ask why. Maybe the answer is excellent. Maybe the answer is "because the open book is already enough risk." Maybe the answer is "because the macro calendar is too dangerous." Maybe the answer is "because the only clean opportunities already passed."

But there should be an answer.

04 - Targets Should Not Always Be The Finish Line

The second part of the lesson was target design.

First targets did their job. They turned valid trades into realized wins. There is nothing wrong with taking the money the plan asked for. A target that gets hit is not a mistake.

But on a strong tape, a full exit at the first target can be too blunt.

Some names do not stop being worth owning simply because the first objective was reached. Sometimes the first target is proof that the thesis worked, not proof that the whole idea is over. The desk needs a way to distinguish between "take the clean win and move on" and "take most of the win, but leave a smaller piece to test whether the day has more to give."

That does not mean every trade deserves a runner. It definitely does not mean a losing position gets magical treatment. In this model, every automated sell still has to respect the no-loss rule.

What it means is that a bullish plan should decide, before the trade fires, whether a partial-runner structure is allowed.

For example: take a majority of the position at the first target, then leave a small remainder with a second target, a review trigger, or a trailing structure that never authorizes a sale below average entry. The exact mechanics matter less than the principle. The plan should know whether first target means "done" or "partly paid, still observing."

Without that decision, the desk keeps relearning the same emotional lesson: the first target protected profit, and the tape kept going.

That is not a reason to stop taking targets. It is a reason to make the target architecture more precise.

05 - The Cash Question

The phrase I want to carry forward is simple:

If the desk is mostly in cash on a confirmed bullish tape, cash needs a thesis.

That thesis can be defensive. It can be smart. It can be the entire reason the system survives a bad week.

But it has to be written down.

The premarket plan should be able to say one of the following clearly:

- We are cash-heavy because the book already contains enough recovery exposure.

- We are cash-heavy because macro risk is too high before a specific event.

- We are cash-heavy because the market is bullish but extended, and we only want pullbacks.

- We are cash-heavy because the watchlist has no A-grade setups.

- We are not cash-heavy; the plan authorizes larger deployment into specific names if confirmation appears.

Those are very different operating postures. They should not all look the same on the dashboard.

This is where the market stack becomes more than decoration. If SPY and QQQ are both constructive, breadth confirms, volatility is calm, and the leading sectors are aligned, the dashboard should not merely say BULL. It should help the desk ask whether the plan's capital posture matches that read.

Not force the trade.

Ask the question.

06 - What Changes Next

The next version of the desk process does not need a new personality. It needs clearer deployment rules.

For A-grade and strong-B names, the morning plan should define both the first entry path and the backup path if the ideal pullback never arrives. If no backup is allowed, the plan should say why. That turns a future miss into an accepted boundary instead of an afternoon argument.

For bullish or fragile-risk-on days, the plan should decide whether partial runners are allowed. If they are allowed, they should be small, explicit, and above-entry only. If they are not allowed, the first target is the finish line by design.

For cash, the plan should set an expectation. If the desk expects to remain mostly liquid, say why. If the market confirms and the plan still refuses to deploy, that refusal should be visible enough to challenge.

And for watch-only names, the desk needs a better vocabulary than "no trade." Some names are true skips. Some are event watches. Some deserve a review after the open. Some deserve a possible amendment if the tape confirms. Those are not the same instruction.

Wednesday made that obvious without punishing the desk for learning it.

That is the best kind of lesson.

The Lesson

The first version of discipline is restraint.

Do not chase. Do not invent trades. Do not let the machine improvise. Do not sell below entry. Do not pretend every green candle is an edge.

That version is working.

The next version of discipline is allocation.

When the market is giving real confirmation, how much of the plan should be allowed to participate? When a first target hits, does the whole trade end or does a small piece keep working? When most of the account is still in cash, is that patience, fear, or an unspoken risk rule?

Those are not philosophical questions. They are desk questions. They decide whether a good read becomes a good day or merely a safe one.

Wednesday did not argue for recklessness. It argued for more explicit conviction.

Cash kept the desk safe.

Now cash needs a thesis.