Notebook 008 - Bull Is Not Permission

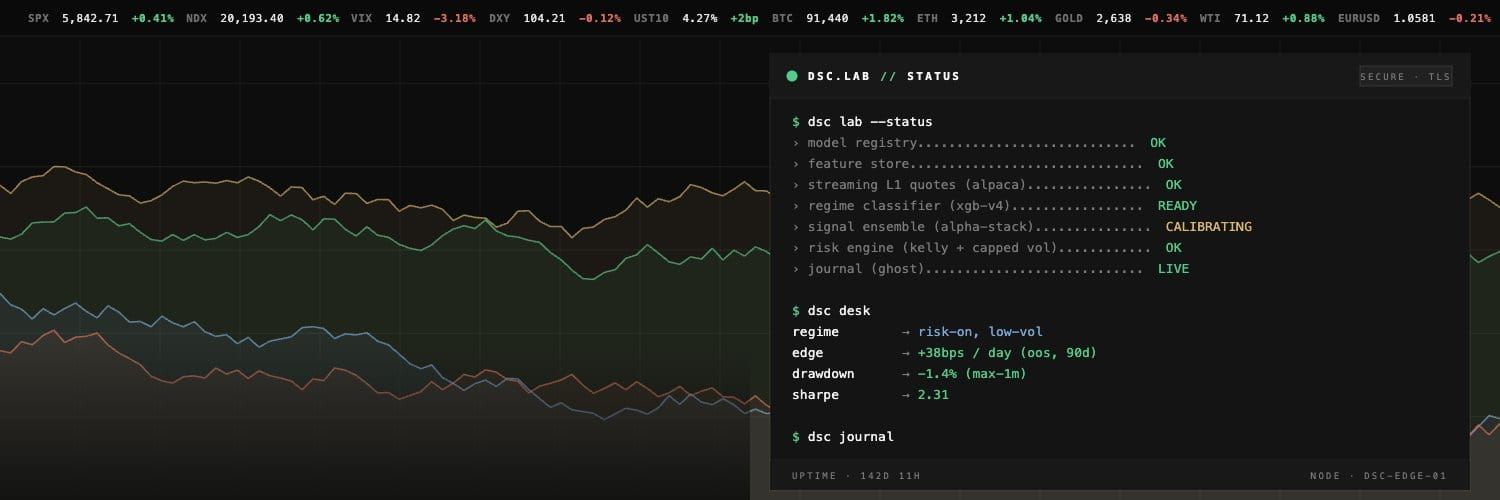

The dashboard said BULL.

That was true. It was not enough.

May 12 was a useful paper-trading day because nothing obvious broke. Onyx was running, the plan was current, the feed was healthy, and the no-loss rule held. The trader did not freelance outside the approved plan. Automated sell orders stayed above average entry. In the basic operating sense, the desk behaved the way it was built to behave.

The lesson came from a subtler place: a bullish regime label after a hot macro print is not the same thing as permission to keep adding fresh risk.

The morning had CPI on it. That matters. Inflation data can change the meaning of the first hour because the market may look strong before it has actually digested what just happened. A green board describes price action. It does not prove the move is durable, broad, or clean enough to lean into.

That distinction showed up in the book.

01 - The Day Was Not A System Failure

The first thing to say is that the system did not fail. This matters because not every red mark in the review is a software problem, and not every missed or faded trade means the rules are wrong.

Onyx followed the approved plan. The no-loss rule remained intact. The open recovery targets stayed above entry. The fresh trades that fired were symbols the plan had authorized. The trader did not decide, on its own, that a bull tape meant every watchlist name deserved a ticket.

That is exactly the baseline we want. A plan-driven system should produce analyzable outcomes. If the day is bad, we should be able to tell whether the plan was wrong, the execution was wrong, or the market changed after the plan was written.

May 12 was mostly the first and third: a risk-posture problem, not an executor problem.

02 - Recovery Management Worked

The cleanest success was not a heroic fresh trade. It was recovery target management.

AAPL came into the day as a carryover position, not a new idea. The important move happened before the open, when the target was reset to a more realistic profit above entry instead of blindly carrying forward the old objective. That is a small wording change with a real behavioral difference. It turns a holdover from dead inventory into an actively managed recovery candidate.

When the tape gave the exit, Onyx took it. That is the no-loss rule working in its most practical form. The system did not sell below entry. It also did not demand a perfect recovery while capital stayed tied up. It accepted a smaller win because the plan had admitted the current tape was not the same tape that created the original target.

That lesson is worth keeping. In a no-loss system, held positions cannot be treated as background clutter. They are the first part of the next plan. Every morning starts with the book we already have, not the book we wish we had.

AMZN and GOOGL made the same point from the other side. Their targets were more realistic than the old carry-forward targets, and they still did not get help from the tape. That does not make the reset wrong. It means recovery targets are necessary but not magic. A damaged hold still needs price confirmation before it stops being damaged.

03 - Fresh Risk Had Mixed Evidence

NVDA was the clean fresh-risk example. It had a plan, the setup appeared, the entry was controlled, and the target was above entry. That matters because the lesson is not "never trade after macro." A strong market after a macro print can produce valid trades. The question is not whether fresh risk is allowed in theory. The question is whether it has earned its way into the book under the actual conditions of the morning.

AMD and TSLA are where the day gets more interesting. They were approved fresh-risk names, and both faded into recovery holds by the close. That does not mean the executor did something wrong. It means the desk posture was too willing to keep treating the session as ordinary risk-on after a macro event that deserved more suspicion.

The same dashboard regime that described a bullish tape did not ask a harder question: is this move strong enough to justify adding more exposure while recovery positions are already on the book?

That is the missing layer.

04 - Bullish Is Not The Same As Durable

The word BULL can be too comforting.

It compresses a lot of information into a simple label. That is useful for scanning, but dangerous if the label starts acting like permission. A market can be bullish and fragile. It can be bullish and crowded. It can be bullish in the index while the names we own or want to trade are giving mixed evidence. It can be bullish for the first thirty minutes and then reveal that the first move was mostly post-print noise.

After hot CPI, the first BULL reading should be treated as provisional.

Not ignored. Not automatically faded. Provisional.

That means the plan needs a second question after the regime label. If SPY and QQQ are up after a hot print, are we full-risk, selective-risk, or target-management-only until the first hour proves itself?

Those are very different trading days.

Full-risk means the macro gate cleared and breadth, leadership, and price action all support fresh entries. Selective-risk means the tape is constructive, but only the cleanest approved names should get capital. Target-management-only means the desk should focus on existing positions and let the first hour pass before adding new exposure.

On May 12, the plan had the language of selectivity. The review showed we needed the enforcement to be louder.

05 - Known Risk Cannot Live Only In Prose

The deeper systems lesson is that known risk cannot sit quietly in the notes while the executor reads a green regime label.

If the morning contains hot macro data, the dashboard should say so in a way the desk cannot miss. If recovery exposure is already meaningful, the plan should show that fresh entries are being throttled because every new entry can become another hold. If the regime flips BULL after a risk event, the dashboard should not simply celebrate the flip. It should ask whether the move is confirmed enough to act on.

This is not about making Onyx more cautious by default. It is about making the system more precise. A desk process should be able to say: the tape is bullish, but the book is heavy; the index is strong, but CPI was hot; the setup is valid, but new exposure is capped; the rally is real, but approval is target-management-only until leadership survives the first hour.

That kind of language protects the operating model. It keeps the trader from freelancing, but it also keeps the human from using a broad label as a shortcut around known risk.

The Lesson

The lesson is not that bullish tapes are fake. Bullish tapes are real. They can produce good trades. May 12 had one. The lesson is that context changes what bullish means.

A clean risk-on morning with an empty book is one thing.

A post-CPI rally with existing recovery positions is another.

The same label can describe both. It should not approve both.

So the rule coming out of the day is simple: BULL is a market description, not a trading authorization. It tells us what the tape is doing. It does not tell us how much risk the desk is allowed to add, how much recovery exposure is already tying up capital, or whether the first-hour move has earned trust after macro.

That question belongs in the plan.

A regime label describes the tape.

It does not approve the trade.