Notebook 007 - When the Tape Outran the Plan

Monday began with a cautious map.

The premarket read was not bearish. It was more restrained than that. SPY and QQQ were not giving a clean directional invitation, the opening posture was selective, and the better entries looked like defined pullbacks rather than early strength. So the plan went into the day with a simple bias: let the best names come back to us, keep size controlled, and avoid paying up for the first move.

That was a defensible plan at 08:30 ET. By late morning, it was no longer the market we were trading.

The tape had changed its mind. SPY and QQQ were pressing higher. High-beta leadership was visible. AI, semis, space, and a few event names were acting like a risk-on basket. Some of the exact names we liked before the open were moving, but they were moving without offering the clean reset the plan required. The dashboard was no longer describing a selective morning. It was describing a bull tape with momentum underneath it.

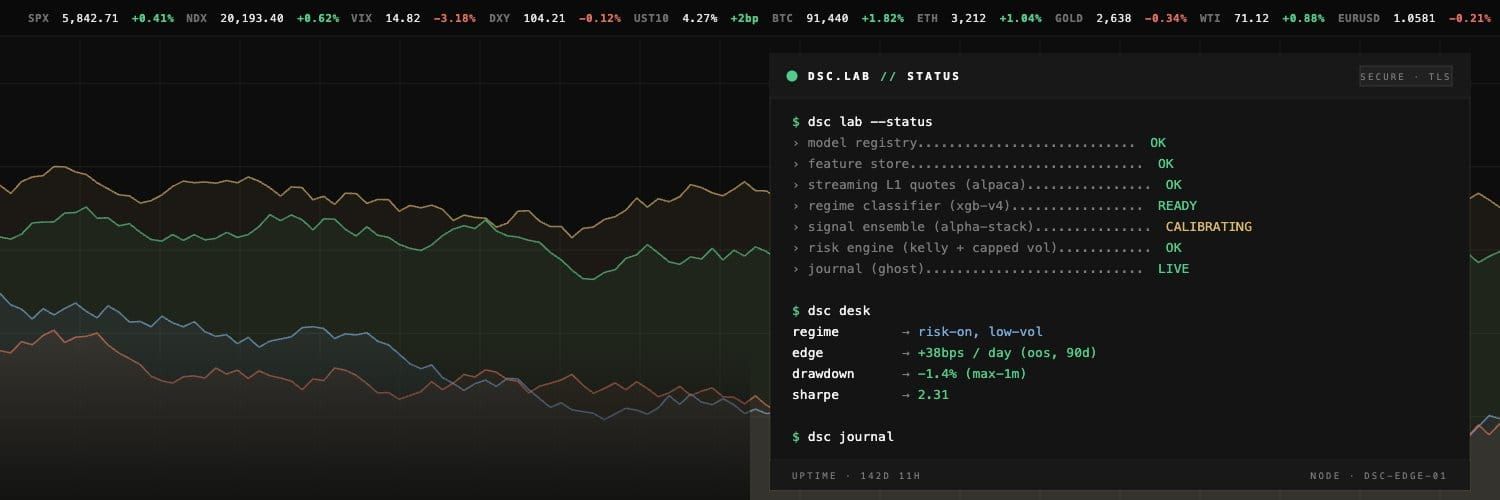

This note comes from a paper-trading environment. It is research, not advice. The useful part of the day is not the profit or the miss. The useful part is that Monday exposed a new layer of the problem: Onyx did not need a looser trader. It needed a better way to translate new information into an approved change while the market was still open.

The Morning Contract

Every morning plan is a contract with the evidence available before the bell. It says, "Based on what we know now, here is what we are willing to do." That contract matters because it keeps emotion from taking over at 09:47 when everything green looks obvious and everything missed looks unforgivable.

Monday's contract was conservative. It preferred price coming back to structure. It treated several names as watch-only. It let a few approved symbols trade if the tape gave a clean entry. On the names that behaved that way, the system was fine. Orders were tied to levels. Targets were above entry. The active book stayed inside the boundaries that were approved.

The problem was not that the morning contract failed immediately. The problem was that it aged quickly.

Markets can do that. A premarket plan is written before the real auction has spoken. Sometimes the open confirms the homework. Sometimes it rejects it. Monday did something subtler: it confirmed the quality of several names while rejecting the entry style chosen for them.

That is a harder miss than being simply wrong.

The Tape Became A Different Document

By midday, the board was sending a clear message. The broad market was firmer than expected. Leaders were extending. Names that had looked interesting but conditional were acting as if the condition had already been satisfied by demand itself. The desk could see it. The dashboard could display pieces of it. The active instructions, however, were still written for the earlier tape.

That is where a trading system can get dangerous in either direction.

One bad answer is to let the machine react on its own. That turns a controlled system into a momentum tourist. It will catch some moves and eventually buy the kind of candle that ruins the week.

The other bad answer is to refuse all adaptation. That keeps the book clean, but it also means the desk can sit there watching a market that has invalidated the morning assumptions while pretending the old assumptions are still enough.

Monday argued for a third path: do not give execution more freedom; give the desk a faster, auditable path from observation to permission.

That sounds bureaucratic until the tape is moving. Then it becomes the difference between discipline and paralysis.

Three Misses That Were Not The Same

The day produced three important misses. They looked similar on the screen: strong names running without Onyx in them. Under the hood, they belonged to three different categories.

The first miss was a unit error. A selected leader had a planned fallback for opening-range strength. The idea was right: if the primary pullback never appeared, a smaller momentum entry could be allowed only if price cleared structure, stayed close enough to that structure, and showed real demand. Replay showed that the setup should have qualified. The trade still did not fire because the system and the plan were not speaking the same unit.

The desk wrote extension caps the way traders speak about them: 1.0 means one percent. Part of the implementation had previously treated decimal-style values differently. That is not a market read. That is a translation bug. The sentence was written correctly, but the reader heard the wrong language.

This is the least romantic kind of trading error and one of the most important to eliminate. A rule can be logically sound and still fail if its representation is ambiguous. Percent points now need to mean percent points everywhere. Suspicious values should be rejected loudly. The dashboard should make the meaning visible enough that a human can see whether the system is enforcing the intended boundary.

The second miss was a missing doorway. One name was marked watch-only in the morning, which made sense before the bell. Once trading started, the stock began validating: structure held, volume mattered, and the move had more substance than a random gap. The executor was correct to leave it alone because the symbol was not approved. But the operating surface had no clean intermediate state between "ignore it" and "manually rewrite the plan while the market is moving."

That is not a code bug. It is a workflow gap. A watch-only name that becomes actionable should be able to generate a proposed amendment: symbol, size, trigger, target, risk note, and the reason the evidence changed. Nothing should trade from that proposal by itself. The proposal should simply put a clean decision in front of the desk while there is still time to make it.

The third miss was the pure runner. This was the one that hurts the most emotionally and teaches the least if we are not careful. The name had a real catalyst. It ran hard. By the time it was clearly working, the entry was already too far away from the structure that would have made it respectable. The normal protections did their job. They said, in effect, "Yes, this is strong, but the price you are being asked to pay is no longer close enough to the reason for the trade."

That kind of miss cannot be fixed by simply loosening the rules. A rule loose enough to catch every vertical move will eventually buy one at the worst possible moment. If Onyx is going to participate in that class of move, it needs a separate trade type written before the open: tiny size, explicit event logic, one entry, no averaging, and no assumption that every fast stock deserves a ticket. If we do not want that category, then those misses have to be accepted instead of relitigated every afternoon.

Those three misses require three different responses: fix the unit, create the doorway, decide whether the runner class exists. Treating them as one generic failure would blur the lesson and make the next version worse.

The Translation Layer

The most important change coming out of Monday is not a new trade signal. It is a new layer of communication.

The dashboard now needs to behave less like a scoreboard and more like an assistant chief of staff. If the broad market flips from selective to BULL, it should say so. If an opening-range setup is valid, it should name it. If a setup is blocked, it should name the blocker instead of letting the desk discover the miss after the fact. If a target fills and the stock keeps running, it should note that continuation. If a watch-only symbol deserves human review, it should ask for a decision in a structured way.

That is why the new alert vocabulary matters. REGIME_FLIP_BULL tells us the market backdrop has changed. OR_MOMENTUM_VALID says an approved backup is alive. OR_MOMENTUM_BLOCKED_RUNNER says strength was present but the entry was too extended or otherwise disqualified. POST_TARGET_RUNNER tells us a profit-taking path may have left money on the table. PLAN_AMENDMENT_REVIEW is the doorway for a human-approved adjustment.

The key word is alert. These messages inform. They do not authorize. The trader still needs an approved instruction before it can act. The difference is that the desk no longer has to rely on hindsight to find out what the tape was offering.

That is a better shape for Onyx. Not more impulsive. More fluent.

What Changes Tomorrow

Tomorrow starts with a slightly different question.

The question is not, "How do we make sure we catch every runner?" That question is a trap. Nobody catches every runner without also catching a lot of trouble. The better question is, "What would have needed to be true before the open for this move to be an approved trade, and what would have needed to change after the open for us to revise that approval?"

That framing keeps the morning work important without pretending the morning is omniscient.

For A-grade and strong B-grade names, the premarket plan should explicitly decide whether an opening-range momentum backup is allowed. If it is allowed, the plan should show the extension cap, VWAP tolerance, time window, and size reduction in plain language. If it is not allowed, the miss is acceptable. No silent second-guessing.

For watch-only names with real catalysts, the plan should name what would earn a review after the open. Not a trade. A review. The distinction matters. The system can say, "This stock has crossed the threshold for human attention," without saying, "Buy it."

For event runners, we need to decide whether a tiny starter class belongs in the model at all. That is a business decision as much as a technical one. If it exists, it must be small enough to survive being early and strict enough not to become a disguised chase. If it does not exist, then a move like Monday's biggest runner is simply outside the game we chose to play.

And for every constraint, the representation needs to be as clear as the idea. A one-percent cap should look like one percent everywhere: in the plan, in validation, in tests, and on the screen.

The Real Lesson

The previous notebooks were about building discipline. Monday was about what happens after discipline starts working.

Once the system stops taking random trades, the misses become cleaner. Once the misses become cleaner, the next problem is not always "more rules" or "fewer rules." Sometimes the next problem is timing. The market gives new evidence while the old decision is still in force. The desk sees the evidence but has no formal way to update the decision quickly enough.

That is the layer Monday exposed.

Onyx should not become a faster hand because the market had a fast day. It should become a better conversation between evidence and permission. The morning plan still matters. The live tape still matters. The review still matters. The work now is connecting those moments without letting any one of them pretend to be the whole truth.

The market outran the morning map. The fix is not to throw away the map.

The fix is to learn how to redraw it while the road is changing.