Notebook 006 - Week One: What Held

This was the first real week of the new operating model. It was a paper-trading week, and this is not financial advice. The point is not whether the desk was up or down. The point is whether the process behaved like a process.

It did. Mostly.

The frame we were testing

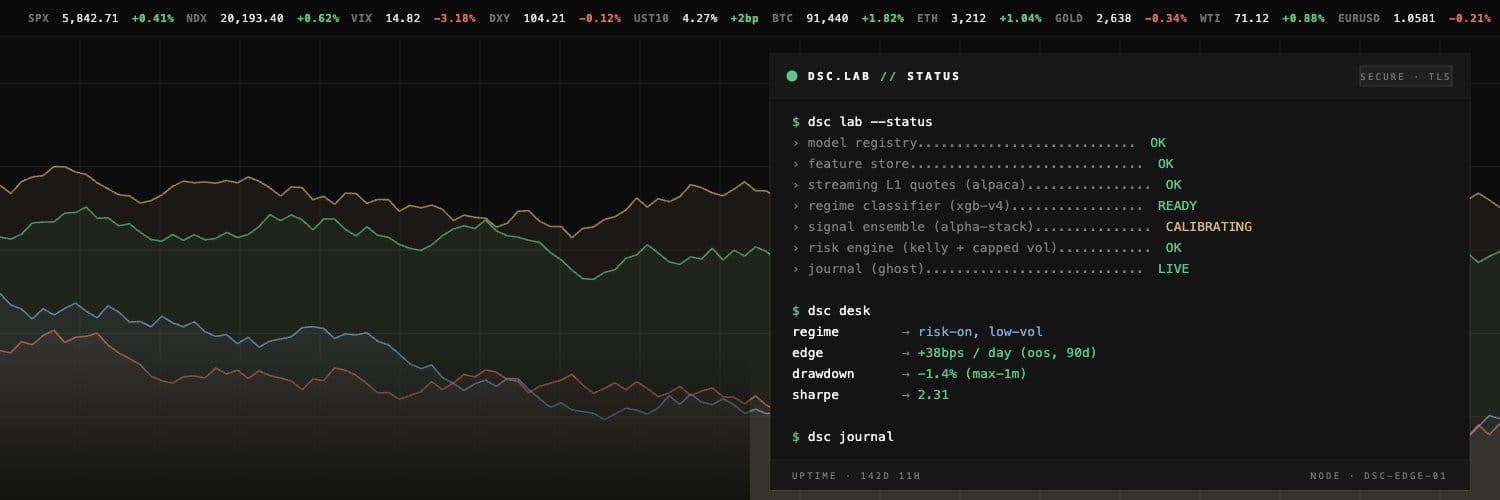

Onyx was not asked to be smart this week. It was asked to be a desk. That distinction matters. A bot is asked to know what to do at any moment. A desk is asked to do the homework, write the plan, execute only the plan, review what happened, and let the next plan get smarter. We have written about that frame before. This week was the first time it ran for a full sequence of days, with positions carrying across sessions, with a real overnight handoff, and with the no-loss rule actually being tested instead of merely respected.

The question for the week was simple. Does the process survive a week of contact with the tape?

Mostly yes.

What held

The daily plan was the edge. The trader did not improvise. It did not equal-weight the watchlist. It did not chase strong names that fell outside the approved list. Every trade Onyx took had a name on the plan, a trigger written down, a target written down, and a reason it existed. Every miss is now categorizable, which is the only reason any of the rest of this writeup is possible.

The no-loss rule held. No automated sell ever fired below the average entry of any position. Not on a stuck name, not on a slow recovery, not on a Friday close into the weekend. That is not a clever achievement. It is the constraint, and the constraint did not break.

Limit-only execution held. Every entry the desk took had a price the desk was willing to pay. There were no market orders, no panic fills, no ambiguity about what the system thought it was doing in fast tape. The audit trail is clean. That is worth more on hard days than on easy ones.

Carry-over discipline held. Open positions from the prior day were treated as the first item of the next premarket session, not as side notes. Targets were re-checked. Underwater holds were named as holds. The plan did not pretend the book was empty just because a new morning had started.

These are unglamorous wins. We will take them.

What did not hold

The week was not clean. It exposed two real problems, and one of them was a problem of our own design.

Pullback-only was too narrow on a strong tape. The plan's preferred entry mode was a pullback to structure. That is conservative on purpose. It keeps the desk from buying the top of a vertical candle just because the chart looks exciting. But in a risk-on week with several leadership names that never gave the discount we asked for, a strict pullback-only posture is a posture that watches the move from the sidelines. That is a real cost. We did not pay it because the system was wrong. We paid it because the system was narrow.

One guardrail blocked the trade it was designed to safely permit. Late in the week, the plan was widened to allow a guarded opening-range momentum backup for a small number of stronger names. The shape was right. The shape required an opening-range structure, a VWAP filter, a market-regime requirement, and smaller size than the primary setup. But the first version of the guardrail used a hard RSI ceiling as its anti-chase protection, and on the cleanest test case of the week the RSI ceiling rejected the entry — not because demand was fake, but because demand was loud. A guardrail that rejects every leader the moment it confirms is not a guardrail. It is a refusal to take the trade you said you would take.

The fix is not to remove the brake. The fix is to aim it. Distance from structure, not absolute strength reading. A leader can be hot and still be only slightly above its opening range. A weaker name can have a tame reading and be wildly extended above VWAP. Those are different risks. The week showed, concretely, why one rule cannot do both jobs.

Two misses that look the same and aren't

The week ended with two missed leadership runs, and from the outside they look identical. Inside the system they were not.

The first was a name where the trade family was authorized in the plan, the structure confirmed exactly the way the plan asked it to confirm, and a single guardrail rejected the entry. That is a guardrail problem. It is fixable in the rule, not in the discretion.

The second was a name where the trade family was not authorized in the plan at all. The desk did not enter, and the desk was correct not to enter, because authorization had to happen at the morning desk, not in the heat of the move. The lesson there is upstream. Either the premarket process should have approved a smaller continuation backup before the open, or it should not have. That is a planning question. It is not the executor's job to second-guess.

We do not want to fix those two misses with the same change. They are different fixes.

What the no-loss rule actually costs

The rule held, and the rule has a cost. We will keep saying that until we are sure we mean it.

A no-loss system does not delete risk. It moves risk from realized P&L into open inventory. A bad entry does not become a small realized loss. It becomes a held position the size of the bad entry, with the desk's cash partly tied up until the position recovers or hits a non-negative target. That is not a free lunch. It is a constraint that forces the rest of the system to behave: smaller starter sizes when conviction is uncertain, real cash reserves, real concentration limits, and an absolute respect for event risk that could turn a small entry into a long hold.

This week, the rule survived contact with the tape because the rest of the system stayed honest about it. The book ended the week with names below entry that we are managing, not names below entry we are pretending are about to fix themselves. That is the version of the rule that works. The version that pretends drawdown is not real is the version that ends careers.

The shape of week two

Week one earned us the right to go into week two with narrower, more honest plan language. A few specific carries:

- The first item of Monday is not a fresh idea. It is position management on the names already on the book, and a check that overnight target orders survived the weekend instead of expiring quietly.

NO_TRADEis too binary for event names. The plan will move towardHARD_SKIP,EVENT_WATCH, andREVIEW_AFTER_OPENso that "not a normal trade" is not the same instruction as "do not look at this stock."- Opening-range momentum stays off by default. Where it is on, it is only on for A-grade and strong-B names, with an extension cap instead of an absolute strength ceiling, with smaller size than the primary setup, and only when the broad market gives permission.

- Late-day low-conviction trades have to be smaller, or have to be explicitly approved, because under a no-loss rule a late C entry is functionally a request to hold overnight.

- Target sells need to be consolidated by symbol and price, and need to be set to honor extended hours, especially on positions held into the weekend.

None of those are flashy. All of them are specific. Every one of them came from a real observation in a real session this week, not from a parameter sweep.

What the week actually proved

We did not prove that the strategy is right. There is no single strategy. We proved something narrower and more useful.

We proved that a daily-plan-driven executor with a no-loss rule can run for a full week without producing random trades, without panic-selling, without manufacturing conviction, and without hiding its mistakes. We proved that the misses the system produced were the kind of misses you can name. We proved that the journal, when used as infrastructure instead of paperwork, is what makes any of this compoundable.

We also proved that constraints have to be honest about their cost. Pullback-only is conservative and incomplete. The no-loss rule protects the desk and ties capital. A momentum backup needs to authorize the move it intends to authorize, or it is theater. None of those statements are interesting alone. Together they are the operating model. The strategy is never the same week to week. The process is.

The process is the strategy. Week one held it.

Now we go again.